Scott is a credit analyst with one of the credit rating agencies in India. He was looking in Oil and Gas Industry companies and has presented brief financials for following 4 entities:  From the data given below, calculate the standard deviation of the credit portfolio assuming that facility's exposure is known with certainty, customer defaults and LGDs are independent of one another and LGDs are independent across borrower(s) . Credit Facility A - Loss Equivalent Exposure of $60m, expected Default frequency of 1.5%, loss given default of 30%, Std Deviation of LGD - 5% and Correlation to portfolio - 0.10 Credit Facility B - Loss Equivalent Exposure of $25m, expected Default frequency of 2%, loss given default of 12%, Std Deviation of LGD - 12% and Correlation to portfolio - 0.45 Credit Facility C - Loss Equivalent Exposure of $15m, expected Default frequency of 5%, loss given default of 85%, Std Deviation of LGD - 18% and Correlation to portfolio - 0.22

From the data given below, calculate the standard deviation of the credit portfolio assuming that facility's exposure is known with certainty, customer defaults and LGDs are independent of one another and LGDs are independent across borrower(s) . Credit Facility A - Loss Equivalent Exposure of $60m, expected Default frequency of 1.5%, loss given default of 30%, Std Deviation of LGD - 5% and Correlation to portfolio - 0.10 Credit Facility B - Loss Equivalent Exposure of $25m, expected Default frequency of 2%, loss given default of 12%, Std Deviation of LGD - 12% and Correlation to portfolio - 0.45 Credit Facility C - Loss Equivalent Exposure of $15m, expected Default frequency of 5%, loss given default of 85%, Std Deviation of LGD - 18% and Correlation to portfolio - 0.22

A) US$6.88 million

B) US$ 1.16 million

C) US$ 1.66 million

D) US$ 0.10 million

Correct Answer:

Verified

Q1: Ms. Mary Brown is a credit rating

Q2: Following is information related banks: Auckland Ltd

Q3: Satish Dhawan, a veteran fixed income trader

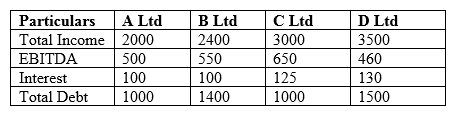

Q4: "Following four entities operate in the Indian

Q6: The longer the term to maturity of

Q7: Scott is a credit analyst with one

Q8: Mr. Gopi, while teaching the CCRA course

Q9: The following information pertains to bonds:

Q10: The following information pertains to bonds:

Q11: Following is information related banks: Auckland Ltd

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents