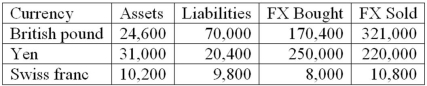

The following are the net currency positions of a Canadian FI (stated in Canadian dollars) .  How would you characterize the FI's risk exposure to fluctuations in the Swiss franc/dollar exchange rate?

How would you characterize the FI's risk exposure to fluctuations in the Swiss franc/dollar exchange rate?

A) The FI is net short in the franc and therefore faces the risk that the franc will rise in value against the U.S. dollar.

B) The FI is net short in the franc and therefore faces the risk that the franc will fall in value against the U.S. dollar.

C) The FI is net long in the franc and therefore faces the risk that the franc will fall in value against the U.S. dollar.

D) The FI is net long in the franc and therefore faces the risk that the franc will rise in value against the U.S. dollar.

E) The FI has a balanced position in the Swiss franc.

Correct Answer:

Verified

Q67: The following are the net currency positions

Q68: Suppose that the current spot exchange rate

Q69: The following are the net currency positions

Q70: The following are the net currency positions

Q73: The one-year CD rates for financial institutions

Q75: The following are the net currency positions

Q83: An FI has purchased (borrowed) a one-year

Q93: Your U.S.bank issues a one-year U.S.CD at

Q99: Your U.S.bank issues a one-year U.S.CD at

Q100: Your U.S.bank issues a one-year U.S.CD at

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents