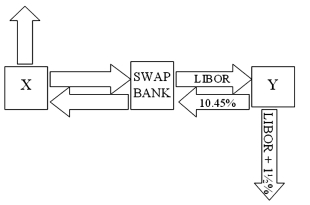

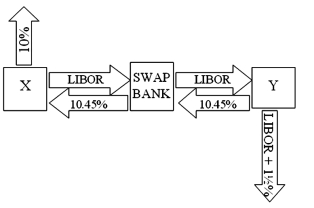

Company X wants to borrow $10,000,000 floating for 5 years; company Y wants to borrow $10,000,000 fixed for 5 years. Their external borrowing opportunities are shown below:  A swap bank is involved and quotes the following rates five-year dollar interest rate swaps at 10.05%-10.45% against LIBOR flat. Assume company Y has agreed, but company X will only agree to the swap if the bank offers better terms.

A swap bank is involved and quotes the following rates five-year dollar interest rate swaps at 10.05%-10.45% against LIBOR flat. Assume company Y has agreed, but company X will only agree to the swap if the bank offers better terms.

What are the absolute best terms the bank can offer X, given that it already booked Y?

A) 10.45%-10.45% against LIBOR flat.

B) 10.45%-10.05% against LIBOR flat.

C) 10.50%-10.50% against LIBOR flat.

D) none of the above.

Correct Answer:

Verified

Q22: Pricing an interest-only single currency swap after

Q23: Consider the dollar- and euro-based borrowing opportunities

Q24: A is a U.S.-based MNC with AAA

Q25: Company X wants to borrow $10,000,000 floating

Q26: Compute the payments due in the FIRST

Q28: In a currency swap

A)it may be the

Q29: Swaps are said to offer market completeness

A)This

Q30: In the problem just previous, company X

A)is

Q31: Compute the payments due in the second

Q32: Company X wants to borrow $10,000,000 floating

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents