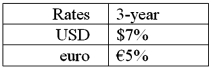

Suppose that you are a swap bank and you notice that interest rates on coupon bonds are as shown. Develop the 3-year bid price of a euro swap quoted against flat USD LIBOR. The current spot exchange rate is $1.50 per €1.00. The size of the swap is €40 million versus $60 million.  In other words, what you be willing to pay in euro against receiving USD LIBOR?

In other words, what you be willing to pay in euro against receiving USD LIBOR?

A) 7%

B) 6%

C) 5%

D) None of the above

Correct Answer:

Verified

Q63: Act as a swap bank and quote

Q66: Devise a direct swap for A and

Q67: What are the IRP 1-year and 2-year

Q69: Come up with a swap (principal +

Q70: With regard to a swap bank acting

Q70: Explain how this opportunity affects which swap

Q71: Suppose that you are a swap bank

Q72: What would be the interest rate?

Q72: What would be the interest rate?

Q73: Suppose that the swap that you proposed

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents