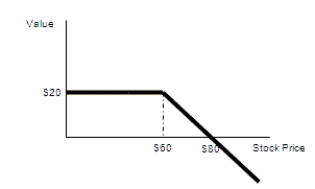

Combining options: Suppose you are creating a portfolio that consists of zero-interest bonds, stock from a single company, and call and put options on the stock. Holding which of the following combination of securities will give the payoff shown in the following diagram?

A) Buy $20 in risk-free bonds, and sell short one call option with a strike price of $60.

B) Buy $20 in risk-free bonds, and buy one put option with a strike price of $60.

C) Buy one share of stock, and buy one call option with a strike price of $60.

D) Buy one share of stock, and sell one put option with a strike price of $60.

Correct Answer:

Verified

Q84: Risk management: Consider a wheat farmer who

Q87: Binomial pricing: Assume that the stock of

Q88: Combining options: Suppose you are creating a

Q90: Binomial pricing: Assume that the stock of

Q91: Binomial pricing: Assume that the stock of

Q93: Binomial pricing: Assume that the stock of

Q94: Binomial pricing: Assume that the stock of

Q95: Binomial pricing: Consider two call options written

Q96: Combining options: Suppose you are creating a

Q97: Binomial pricing: Assume that the stock of

Unlock this Answer For Free Now!

View this answer and more for free by performing one of the following actions

Scan the QR code to install the App and get 2 free unlocks

Unlock quizzes for free by uploading documents